For many families in San Diego and across Southern California, the cost of higher education can feel overwhelming. Tuition continues to rise at universities across the country, and even in-state public schools can represent a significant financial commitment. While scholarships, grants, and savings can cover part of the expense, many students rely on loans to bridge the gap.

Borrowing for college is not necessarily a bad decision. Education is often one of the most valuable long-term investments a student can make. The key is to approach borrowing thoughtfully and to understand the long-term impact before signing loan agreements.

Families that take time to evaluate their options, compare financial aid offers, and calculate realistic repayment scenarios tend to avoid the common pitfalls associated with excessive debt. Planning early gives students more flexibility and helps ensure their education supports future career goals rather than creating financial stress.

A thoughtful approach to financing college begins long before the first tuition bill arrives. It involves researching costs, understanding financial aid packages, and developing a strategy that balances opportunity with affordability.

Understanding the True Cost of a College Degree

When students consider the price of college, they often focus only on tuition. However, the real cost of attending school includes many additional expenses that can quickly add up.

Housing, meal plans, textbooks, transportation, and personal expenses all contribute to the overall cost of attendance. For students attending universities in California, especially in coastal or other urban areas, housing can be one of the largest expenses.

In Southern California, students choosing schools in cities like San Diego, Los Angeles, or Irvine often face higher living costs than the national average. This reality makes it essential for families to calculate a full budget before committing to a particular school.

Another factor to consider is how costs may increase over time. Tuition often rises annually, and students typically attend school for four years or more. Planning with potential increases in mind helps avoid financial surprises during later years of study.

By understanding the complete financial picture, families can make more informed decisions about which schools provide the best balance between academic opportunity and financial sustainability.

Choosing Loans That Work in Your Favor

Not all loans are created equal. Some offer more favorable terms, lower interest rates, and better repayment options than others.

Federal loans are typically the first option families should consider. These loans often provide fixed interest rates, flexible repayment plans, and protections such as income-driven repayment or temporary deferment if financial challenges arise.

Private loans, on the other hand, are usually offered by banks or financial institutions. While they may help cover remaining expenses, they often come with higher interest rates and fewer borrower protections. Because of this, many financial advisors recommend exhausting federal loan options before considering private lenders.

Understanding interest rates is especially important. Even small differences in rates can significantly affect how much borrowers pay over time. Families who compare loan terms carefully often save thousands of dollars over the life of the loan.

Another important strategy is to borrow only what is necessary. While loan offers may appear generous, accepting the maximum amount is not always the best decision. Responsible borrowing focuses on realistic repayment expectations after graduation.

Building a Practical Budget for College Years

Budgeting plays a major role in keeping education costs under control. Students who develop good financial habits early are more likely to graduate with manageable debt and stronger money management skills.

A practical college budget begins with understanding income sources. These may include scholarships, grants, family contributions, part-time work, and financial aid. Once income is clear, students can evaluate how much of their expenses must be covered through borrowing.

Living arrangements often make a big difference. Students who live at home during the first year or two may dramatically reduce housing costs. Community college transfer pathways are another option that many Southern California families consider to reduce overall education costs.

Daily spending habits also matter. Small expenses such as food delivery, rideshare services, and subscriptions can add up quickly over a semester. Tracking these expenses helps students stay aware of their financial limits.

Creating a simple monthly budget encourages responsible decision-making and prevents unnecessary borrowing. Over time, these habits support long-term financial independence.

Preparing for Repayment Before Graduation

Many students think about loan repayment only after they graduate, but planning earlier makes the process far less stressful.

Understanding how repayment works helps students estimate their future financial obligations. Monthly payments typically begin several months after graduation, and the total amount paid depends on the loan size, interest rate, and repayment term.

Students who expect to pursue careers in fields such as education, healthcare, public service, or nonprofit work may also qualify for loan forgiveness programs or income-driven repayment plans. These programs can significantly reduce the burden of repayment over time.

Another strategy involves making small payments while still in school. Even paying interest during enrollment can prevent loan balances from growing larger due to capitalization.

Career planning also plays an important role. Students who research expected salaries in their chosen field can better determine how much borrowing is reasonable. Aligning loan amounts with realistic income expectations creates a safer financial future.

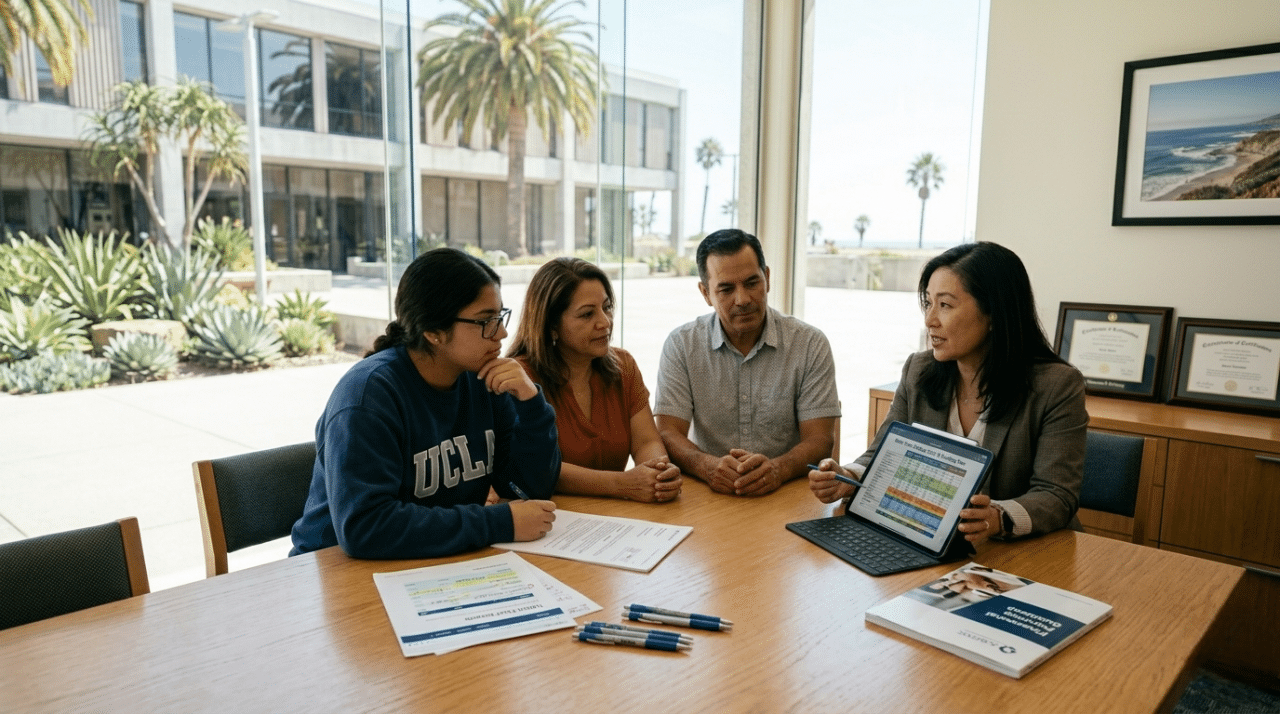

Getting Professional Guidance When Needed

For many families, the college financing process can feel confusing and overwhelming. Financial aid letters, loan terms, and repayment options are not always easy to interpret without guidance.

Professional advisors who specialize in college financial planning help families evaluate their options and make informed decisions. They often assist with comparing financial aid packages, identifying scholarship opportunities, and building realistic borrowing strategies.

In regions like San Diego and throughout Southern California, where college-bound families often face high living costs and competitive admissions environments, expert guidance can provide clarity and peace of mind.

Working with an experienced advisor allows families to avoid common mistakes, such as overborrowing, misunderstanding loan terms, or missing opportunities for financial aid.

Ultimately, a thoughtful approach to financing education allows students to focus on what matters most—gaining knowledge, developing skills, and preparing for a successful future without unnecessary financial stress.

At College Planning Source, we help students and families navigate every step of the college admissions process. Get direct one-on-one guidance with a complimentary virtual college planning assessment—call 858-676-0700 or schedule online at collegeplanningsource.com/assessments.